"The yield on 1-year Greek government debt ended last week at 110%, down slightly from a mid-week peak of 130%. Even with the pullback, the Greek yield structure continues to imply default with certainty. All the markets are really quibbling about here is the recovery rate - what percentage of face value investors can expect to obtain post-default. That figure was still hovering near 50% as of Friday, but was a bit higher than we saw a few days earlier.

Despite a Greek 1-year yield that is already over 100%, it is still possible to kick the can down the road for another few months with another bailout, but the costs of that would now be extraordinarily high because of the low expected recovery rate. Much better to provide the funds to a post-default Greece, or to use them to recapitalize the banking system after losses that now appear inevitable.

Doureios Ippos: Greek 1-year yields

Equo ne credite, Teucri! Quidquid id est, timeo Danaos et dona ferentes*

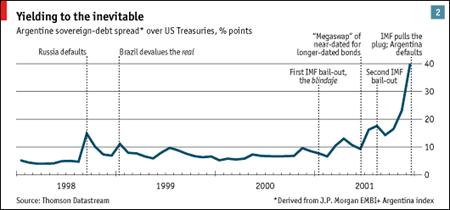

As a refresher on how all of this works, the following chart appeared years ago in the Economist, a chronicle of the frantic bail-outs in the months preceding the default of Argentine debt (which amounted to about $81 billion. Needless to say, the numbers involved in a potential Greek default are much larger, but the pattern we are seeing in Greece is identical to the signature of other historical sovereign defaults (see Uruguay, Russia and other countries as well ) - a sustained rise in yields, coupled with official statements about the "impossibility" of default, multiple bailout efforts that quickly fail, culminating in a vertical spike in yields (toward the inverse of the expected recovery rate, minus 1).

The case of Argentina is instructive because it was in a situation much like that of Greece. Argentina's currency was both pegged and officially convertible into the U.S. dollar, and most of Argentina's debt was denominated in U.S. dollars, creating a situation where its debt burden was in the form of a currency that it effectively could not print. The subsequent default was accompanied first by an abrupt devaluation of the peso to a new peg, and eventually to complete abandonment of the pegged exchange rate.

From the history of sovereign defaults, we can already create something of a roadmap of the financial crisis that appears about to unfold, and the associated choices involved.

Suppose first that Greece agrees to implement new austerity measures and receives another tranche of bailout funding. We already know that applying severe budget austerity in an economy that is in depression (as Greece essentially is) does not materially close the budget deficit, but instead produces further economic weakness and revenue shortfalls. The past year has been a clear example of that. By the end of the year, even with new bailout funding, Greece will have a debt-to-GDP ratio approaching 180%. This is an impossible debt burden to service, and would be even if interest rates in Greece were only a few percent. New bailout funding here means that we'll observe more rioting in Greece as new austerity measures are implemented, the Greek economy will largely shut down, and within a few months, we'll be facing the default issue again but at an even higher debt-to-GDP level and even lower anticipated recovery rates.

Thus, a bailout today does not avert default, but at best defers it to a later date, and squanders funds that could otherwise be used to stabilize the European banking system once that inevitable default occurs.

Of course, there is the implausible option for stronger countries such as France and Germany to literally pay off half of the government debt of Greece, taking those debt burdens upon themselves. But this clearly would not be tolerable politically, and would invite similar expectations from other teetering Euro-zone countries such as Portugal, undoubtedly also encouraging them to completely abandon any remaining fiscal discipline.

So Greece will default, either now or within several months. In response, three actions will be critical: preventing contagion, preserving the euro, and stabilizing the banking system."

http://www.hussman.net/wmc/wmc110919.htm

No comments:

Post a Comment